I take no pleasure in this prediction. I am not a vegan, nor do I have any strong wish to become one. And yet, I think a lot of people will be vegans in the near future for simple reasons of technology, cost, and environmental sustainability.

A popular talking point among vegans is that a calorie of animal product is much more expensive in terms of land, labor and energy resources to produce than a calorie of plant food. And this is true. It's certainly less efficient to grow corn, feed it to a cow, and then eat the cow. Cut out the middle cow and eat the corn directly! But of course, corn (and any other plant) doesn't taste like cow, and to date the rich West has been willing to pay the premium necessary to purchase the flavor and texture of meat.

Several trends however are coming together which I think will move a substantial amount of our consumption away from animal products towards plant products. From there, changes in politics will finish off animal farming as a major industry.

The first trend is merely the limitation of land resources. Already, 26% of the Earth's surface is devoted to grazing, and 1/3 of our arable land is used to grow crops fed to food animals. I don't know what the Earth's sustainable level of beef production is, but seeing how over-grazing is already a severe problem in some areas, it may well be less than the level we have now. Combine this fixed supply with a growing population and we should expect the price of animal products to rise over time.

The second trend is the improving sophistication of "fake" animal products. Muufri is making "animal free" milk that matches real cow milk protein-for-protein and fatty-acid-for-fatty-acid, just from plant sources. Impossible Foods is doing the same for meat, even going so far as to replicate the hemoglobin in blood from plant sources. The promise of both of these companies, and others working in the same field, is to deliver plant-based products which are indistinguishable from their animal-based counterparts, but at lower cost. Already in blind experiments, according to Impossible Food's research, professional chefs are unable to tell the difference between their products and the real thing during preparation and cooking, and customers can't tell the difference either. And the product is improving from there, since they have precise control over the chemistry. This isn't your uncle's tofu burger.

The third trend is the direct manipulation of DNA using technology like CRISPR. In 2013, the biotech startup Pronutria came out of stealth and David Berry (one of their founders) gave a Google Solve For X talk on their technology. Basically, they created a library of single-celled creatures and DNA tools for modifying them to create the amino acids and vitamins necessary for human health from a continuous process algae farm. Pronutria observed that by growing these nutrients directly from algae we can provide all of the non-calorie nutrient needs (proteins and vitamins, excluding starch and fat) of the entire planet from a non-arable patch of land (or calm ocean water) the size of Rhode Island. Obviously the fresh water and energy requirements are also much lower than standard agriculture.

Taken together, the above three trends say that the costs of animal products will rise, the quality and price of their plant-based substitutes are already near-equal, and the energy and resource cost of plant-based substitutes are already lower and destined to fall much further. Over time the competitive bidding for a good steak from the global rich will drive up the cost of fixed-supply "real" meat, while simultaneously scalable biotech alternatives will come to enjoy economies of scale and learning curves, driving down their prices towards the marginal cost of energy and non-arable land (low).

Will animal farming simply go away? Not immediately. There will certainly be many people who don't want to give up their animal-based foods, and will be able to afford to keep eating it. But there's 4 billion people in Asia who want to eat well, and by the end of this century there may be just as many in Africa. There simply isn't enough grazing land on Earth to feed everyone real meat, and given a sufficiently tasty substitute (which may be even more nutritious than the real thing), the world's poor and middle class will probably go for it. Over time, as more people get used to the idea of plant-based meat and dairy products, political acceptance of the known downsides of standard agriculture (the environmental and ethnical issues surrounding animal welfare) will dry up. I can see a future where so many of the voting public becomes disconnected from eating animal-based meat that it acquires a reputation similar to fox hunting - something vaguely cruel and pointless that only eccentric rich people do. Regulations that make it increasingly expensive and rare would follow quickly from that point, in the name of animal welfare or environmental protection.

On the plus side, for those of you currently saddened by the thought of never having a "real" hot pastrami sandwich in the post-meat future, any real limit on Earth's human-population carrying capacity will be expanded out into the indeterminate future by the events described in this post. Malnutrition will be abolished anywhere supply chains and markets are reasonably functional, and we will become infinitely richer in the ultimate resource. So we'll have that going for us, which is nice.

Thursday, May 28, 2015

Wednesday, May 20, 2015

Solar panels aren't computer chips

Much hay has been made in the last couple years of the steep price declines in solar panels. Here's a typically excitable piece by Noah Smith. The excitement of these posts seems to be driven by the expectation of exponential technological improvement over time. As Noah concludes:

Solar panels are a bulk-manufactured commodity. They aren't terribly hard to make; Elon Musk described them as being slightly simpler to make than drywall panels. And that's true. What's relevant to predicting the future of solar though is that no one predicts drywall panels to get 7% cheaper per year indefinitely. It's understood that their price is a function of their basic costs in terms of material, labor, and energy inputs, and that this can only be asymptotically approached, but not passed through (barring a technological substitute of some sort).

Batteries are similarly bulk-manufactured commodities. That's why Elon Musk isn't relying on Intel to deliver him cheaper batteries each year. He's building the Gigafactory instead because economies of scale are the only way to drive down bulk-manufactured commodity prices in the short-run. Technological price decreases happen at a much slower rate in this sector, when they happen at all. The same economies of scale are why Solar City bought Silevo and plan to product a 1 GW/year production plant in New York.

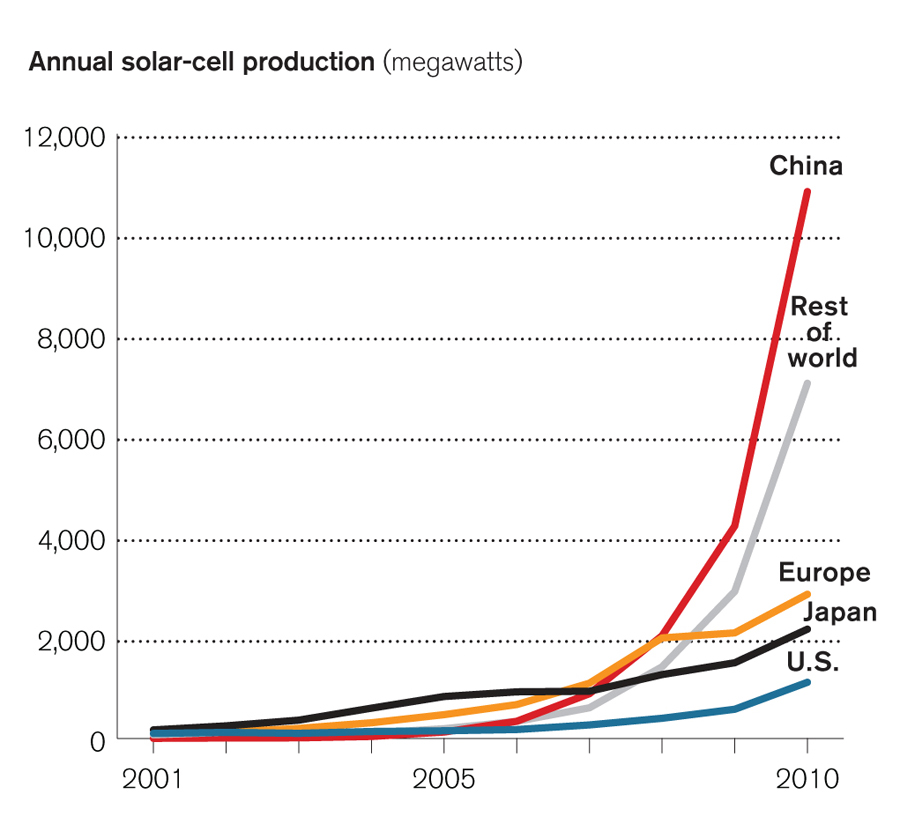

So will Gigafactories help make solar panels cheaper? Yes, but only once - and it already happened. The solar panel gigafactories were built in China. I'm going to show you a chart now and let you guess when they were built:

This huge build-out in industrial capacity is what drove down prices. However, there was over-investment (Over-investment in China?!?! Sacre bleu!) and the spot price of solar panels were driven below production costs, leading to massive losses. Now the butcher's bill is getting paid.

This huge build-out in industrial capacity is what drove down prices. However, there was over-investment (Over-investment in China?!?! Sacre bleu!) and the spot price of solar panels were driven below production costs, leading to massive losses. Now the butcher's bill is getting paid.

The #1 solar panel module maker in the world is Yingli, but they got there by selling their panels at a loss for the last four years, and now they're on the verge of bankruptcy. Baoding Tianwei, a State-owned firm in China that is a supplier to solar companies, has defaulted on its bonds, blaming the glut of supply in the solar market. These two firms are not alone, I'm sure.

There will be a retrenchment in the production of solar panels as firms exit the business. Supply will contract until it meets up with demand again and the producers are profitable. The steep price declines we have seen in the last ten years won't be totally reversed, but they won't be totally kept either. Not in the short term.

So is there hope for future price declines? Sure, as long as you keep your expectations modest. The Solar City-Silevo merger I mentioned earlier is basically a technology play, relying on Silevo's superior technology to improve solar efficiency at the same price as today's panels. That's a good thing, and the price per watt will fall from that. But we shouldn't expect exponential curves in this industry. It's going to be a long, hard, slog.

The takeoff of solar-plus-batteries has only begun to ramp up the exponential curveI don't think this is the correct point of view. There is only one technology which is riding an exponential curve, and that's the miniaturization of electronics. Each time the feature size of a chip or memory register shrinks, the density of compute, memory and storage increases at an exponential rate. But most technologies don't work this way, and solar (despite being made from silicon) is not riding that curve.

Solar panels are a bulk-manufactured commodity. They aren't terribly hard to make; Elon Musk described them as being slightly simpler to make than drywall panels. And that's true. What's relevant to predicting the future of solar though is that no one predicts drywall panels to get 7% cheaper per year indefinitely. It's understood that their price is a function of their basic costs in terms of material, labor, and energy inputs, and that this can only be asymptotically approached, but not passed through (barring a technological substitute of some sort).

Batteries are similarly bulk-manufactured commodities. That's why Elon Musk isn't relying on Intel to deliver him cheaper batteries each year. He's building the Gigafactory instead because economies of scale are the only way to drive down bulk-manufactured commodity prices in the short-run. Technological price decreases happen at a much slower rate in this sector, when they happen at all. The same economies of scale are why Solar City bought Silevo and plan to product a 1 GW/year production plant in New York.

So will Gigafactories help make solar panels cheaper? Yes, but only once - and it already happened. The solar panel gigafactories were built in China. I'm going to show you a chart now and let you guess when they were built:

The #1 solar panel module maker in the world is Yingli, but they got there by selling their panels at a loss for the last four years, and now they're on the verge of bankruptcy. Baoding Tianwei, a State-owned firm in China that is a supplier to solar companies, has defaulted on its bonds, blaming the glut of supply in the solar market. These two firms are not alone, I'm sure.

There will be a retrenchment in the production of solar panels as firms exit the business. Supply will contract until it meets up with demand again and the producers are profitable. The steep price declines we have seen in the last ten years won't be totally reversed, but they won't be totally kept either. Not in the short term.

So is there hope for future price declines? Sure, as long as you keep your expectations modest. The Solar City-Silevo merger I mentioned earlier is basically a technology play, relying on Silevo's superior technology to improve solar efficiency at the same price as today's panels. That's a good thing, and the price per watt will fall from that. But we shouldn't expect exponential curves in this industry. It's going to be a long, hard, slog.

Tuesday, May 19, 2015

21 -- Part 2

My thinking on 21 has evolved a little bit over the first 24 hours. I'm going to lay out three scenarios for how I see the possibilities here.

First, to recap -

Subsidies, Revenue Sharing. This is the bait. Manufacturing electronics is a famously low-margin business. Margins on RAM or chips are razor-thin, and the ability to eek out even another 1% of margin will be leapt at. The sales pitch here is easy for getting the chip included in devices. "Hey, manufacturers, how would you like to earn a perpetual revenue stream from your devices?" It's almost free money to them.

With fast manufacturer and distribution uptake, consumers will end up with devices with this functionality whether they want it or not. It'll just be there, and the revenue splitting will be done by 21 (not the device). Even if there are ways for consumers to turn it off or modify the functionality (likely requiring jail-breaking the device), most won't.

Meanwhile consumers will see higher electric bills, but probably not so much higher they'll really care. They'll just see a status indicator that they have 50 Satoshis in their wallet, or whatever.

Priming the Pump: With fast manufacturer and distribution inclusion, and a 2-3 year upgrade cycle in mobile phones, we could have 21 BitShare chips in every mobile device in the world within a couple years. This lays the groundwork for massive developer support of the new features this allows.

However, for that to happen, 21 needs to protect the consumer's revenue split from greedy manufactures and distributors. If the manufacturer can take 100% of the Satoshis that aren't taken by 21, then the end-user gets nothing, and the potential for having automatic BTC just magically appear in their hardware wallet evaporates.

This leads to three scenarios:

GOOD

21 sees the opportunity to be the "AOL CD" of Bitcoin. Back in the 1990s average folks didn't know what the Internet was, or what it was for, or why they needed it, and it was hard for AOL to market their product, so their solution was to rain down Biblical plagues worth of free trial CDs on the people. Literally everyone in America ended up with a free trial CD (or a dozen of them) whether they wanted one or not, and a number of them put it into their computer on a "Why the hell not?" basis.

This could be a similar situation. Because of the financial incentive to manufacturers to include the 21 BitShare chip in every device, the public gets BTC on their mobile devices whether they want any or not. And each week or month a few of them will start using them on the same "Why not?" basis. This strategy is about getting BTC in front of as many people as possible to bootstrap Bitcoin to being the global financial protocol its boosters claim it's capable of being.

This scenario accepts that people won't voluntarily buy phones with BTC and load them up with Satoshis, mostly due to a lack of consumer education, but believes that the value is there if they can just get people to use it. Obviously this depends on the authentication and smart contract value of having a few Satoshis on hand actually being valuable to consumers. Because if it isn't, all they get is costs.

EVIL

21 sees the opportunity to control a very large mining pool, and they're offering a cut of those profits to all manufacturers and distribution channels, and getting unsuspecting consumers to pay for it with "free" electricity. This way 21 can undercut the mining cost structure of all the other professional miners who have an electric bill they need to pay.

Consumers get a slightly cheaper device (maybe), but there's no minimum reward-split for the end-user; all they get out of this scenario is slightly higher electric bills. The smart contracts features never appear, or they appear but the manufacturer takes 100% of the BTC earned, so the end-user never has any BTC to sign smart contracts with. There's no benefit to end-users here. It's hoped by 21 that the electric bill cost bump will be low enough to be a "tolerable annoyance", rather than something painful enough for consumers to revolt over.

NECESSARY EVIL

This scenario recognizes that both the GOOD and EVIL scenarios are real, but the EVIL scenario is seen as an intermediate stage to a future where consumers become educated about Bitcoins, want Bitcoins, and demand devices that share the majority of their mining rewards with the end-user, and not the distribution channel or even with 21. Also the mining chip eventually takes a back seat to the real feature that allows IoT commerce - hardware wallets in everything.

This scenario also contemplates that 21 won't be able to stamp out all other miners, so we don't have to worry about a 51% attack in the network. If the strategy is successful, competitors will appear en masse. It's not like ASIC mining chips are hard to design. Compared to a CPU or GPU, they're dirt simple. Some Chinese firms will reverse engineer the features necessary to work with whatever standards 21 has developed, and will sell those chips at a pittance. The mining pools will be as fragmented as the companies selling these chips. The share of revenue going to the chip companies will be driven down to the minimum viable margin, and it only remains to be seen whether the lion's share of the rewards go to the distributors or the end-users. Ultimately we end up in a place where every device in the world contributes a little hashing power to securing the network, and a 51% attack is physically impossible even by adversaries as well funded as the US or Chinese governments.

BUT WHICH IS IT?

Heck if I know. Frankly, reading the launch blog post by the CEO of the company, I can't help but be dismayed by how poorly written it is and how many logical inconsistencies it contains. It's a very bad start, and suggests either that they're really disorganized and have no idea what they're doing, or are actively trying to deceive people. Or maybe they're just really, really bad at explaining themselves. Who knows. We will have to wait and see what sort of contracts they actually strike in the manufacturing sector.

First, to recap -

- 21 has built a single-core mining ASIC that can be embedded in any electronic or home appliance. So if your mobile phone is plugged in, fully charged, and on Wifi, it can do some hashing and contribute to a virtual mining pool operated by 21 (I'm assuming they have the sense to not run mining operations while you're out and about, killing battery life and using up your data). This will produce a small stream of Satoshis for the device's use.

- The 21 Chip's mining process would be most cost-efficient in appliances that need to generate heat anyway, such as slow-cookers or washing machines. The chip can just be part of the heating element. But would Satoshis in your rice cooker be useful? I would think they'd be most useful in interactive devices such as your phone, tablet, home PC, or smart TV, so the economics are worse.

- The 21 Chip's mining process will never be as efficient as running your own (or hosted) mining rig in a low-cost electricity market, because of revenue splitting and local variance in the cost of electricity. Essentially you're spending $4 in electricity to get $1 in BTC. The $3 is the "cost" of having automatic, embedded Bitcoin in all of your devices. Convenience over frugality.

- Revenue splitting isn't just between the user and 21, but also allows for payments to be made to the manufacturer the chip is in, as well as the distribution channel. 21 specifically mentions the ability for retailers or mobile carriers to configure the 21 Chips they sell such that they earn BTC over time from a user's mining activity. The actual revenue split isn't disclosed. Does 21 guarantee a minimum share of income to the end-user? That's not clear.

- There is the possibility that devices will be able to use their Satoshis for authentication and identification. Of all the features mentioned in the 21's blog post, this is the only one that promises any real value to consumers.

Well, at 21 we are less concerned with bitcoin as a financial instrument and more interested in bitcoin as a protocolAnd this:

Crucial to this is the idea that bitcoin generated by embedded mining is more convenient — and hence more valuable — than bitcoin bought at market price and manually moved over to the site of utility.

These statements seem to concede my point #3 above, which is that the BTC generated by these devices will be peanuts-small and obscenely expensive compared to just running a mining rig. How much can a mobile carrier really make off of a cheap smartphone in the developing world? A couple dollars per year, at most? That's hardly enough to meaningfully defray the costs of a new electronic device.

I take them at their word that they consider BTC more useful as a protocol than as a financial instrument. Especially at the Satoshi price level! But what to make of all the space they spend on making arguments about payment streams or making micro-payments for things? Would the average user even care about the ability to buy, mayyyybe, one free song per month from their mining rewards? I have my doubts.

Meanwhile, this quote indicates a deeper purpose, about changing the basic fabric of computing:

Conceptually, we believe that embedded mining will ultimately establish bitcoin as a fundamental system resource on par with CPU, bandwidth, hard drive space, and RAM.And:

Towards that end, our team of PhDs in EE from MIT, Stanford, and CMU has built not just a chip, but a full technology stack around the chip — including reference devices, datasheets, a cloud backend, and software protocols.So here's what I think: I think we are looking at a classic bait & switch, but I'm not sure yet whether the intended patsy is the consumer or the manufacturing sector. Which one it will determine whether 21 is a "good" company or an "evil" one.

Subsidies, Revenue Sharing. This is the bait. Manufacturing electronics is a famously low-margin business. Margins on RAM or chips are razor-thin, and the ability to eek out even another 1% of margin will be leapt at. The sales pitch here is easy for getting the chip included in devices. "Hey, manufacturers, how would you like to earn a perpetual revenue stream from your devices?" It's almost free money to them.

With fast manufacturer and distribution uptake, consumers will end up with devices with this functionality whether they want it or not. It'll just be there, and the revenue splitting will be done by 21 (not the device). Even if there are ways for consumers to turn it off or modify the functionality (likely requiring jail-breaking the device), most won't.

Meanwhile consumers will see higher electric bills, but probably not so much higher they'll really care. They'll just see a status indicator that they have 50 Satoshis in their wallet, or whatever.

Priming the Pump: With fast manufacturer and distribution inclusion, and a 2-3 year upgrade cycle in mobile phones, we could have 21 BitShare chips in every mobile device in the world within a couple years. This lays the groundwork for massive developer support of the new features this allows.

However, for that to happen, 21 needs to protect the consumer's revenue split from greedy manufactures and distributors. If the manufacturer can take 100% of the Satoshis that aren't taken by 21, then the end-user gets nothing, and the potential for having automatic BTC just magically appear in their hardware wallet evaporates.

This leads to three scenarios:

GOOD

21 sees the opportunity to be the "AOL CD" of Bitcoin. Back in the 1990s average folks didn't know what the Internet was, or what it was for, or why they needed it, and it was hard for AOL to market their product, so their solution was to rain down Biblical plagues worth of free trial CDs on the people. Literally everyone in America ended up with a free trial CD (or a dozen of them) whether they wanted one or not, and a number of them put it into their computer on a "Why the hell not?" basis.

This could be a similar situation. Because of the financial incentive to manufacturers to include the 21 BitShare chip in every device, the public gets BTC on their mobile devices whether they want any or not. And each week or month a few of them will start using them on the same "Why not?" basis. This strategy is about getting BTC in front of as many people as possible to bootstrap Bitcoin to being the global financial protocol its boosters claim it's capable of being.

This scenario accepts that people won't voluntarily buy phones with BTC and load them up with Satoshis, mostly due to a lack of consumer education, but believes that the value is there if they can just get people to use it. Obviously this depends on the authentication and smart contract value of having a few Satoshis on hand actually being valuable to consumers. Because if it isn't, all they get is costs.

EVIL

21 sees the opportunity to control a very large mining pool, and they're offering a cut of those profits to all manufacturers and distribution channels, and getting unsuspecting consumers to pay for it with "free" electricity. This way 21 can undercut the mining cost structure of all the other professional miners who have an electric bill they need to pay.

Consumers get a slightly cheaper device (maybe), but there's no minimum reward-split for the end-user; all they get out of this scenario is slightly higher electric bills. The smart contracts features never appear, or they appear but the manufacturer takes 100% of the BTC earned, so the end-user never has any BTC to sign smart contracts with. There's no benefit to end-users here. It's hoped by 21 that the electric bill cost bump will be low enough to be a "tolerable annoyance", rather than something painful enough for consumers to revolt over.

NECESSARY EVIL

This scenario recognizes that both the GOOD and EVIL scenarios are real, but the EVIL scenario is seen as an intermediate stage to a future where consumers become educated about Bitcoins, want Bitcoins, and demand devices that share the majority of their mining rewards with the end-user, and not the distribution channel or even with 21. Also the mining chip eventually takes a back seat to the real feature that allows IoT commerce - hardware wallets in everything.

This scenario also contemplates that 21 won't be able to stamp out all other miners, so we don't have to worry about a 51% attack in the network. If the strategy is successful, competitors will appear en masse. It's not like ASIC mining chips are hard to design. Compared to a CPU or GPU, they're dirt simple. Some Chinese firms will reverse engineer the features necessary to work with whatever standards 21 has developed, and will sell those chips at a pittance. The mining pools will be as fragmented as the companies selling these chips. The share of revenue going to the chip companies will be driven down to the minimum viable margin, and it only remains to be seen whether the lion's share of the rewards go to the distributors or the end-users. Ultimately we end up in a place where every device in the world contributes a little hashing power to securing the network, and a 51% attack is physically impossible even by adversaries as well funded as the US or Chinese governments.

BUT WHICH IS IT?

Heck if I know. Frankly, reading the launch blog post by the CEO of the company, I can't help but be dismayed by how poorly written it is and how many logical inconsistencies it contains. It's a very bad start, and suggests either that they're really disorganized and have no idea what they're doing, or are actively trying to deceive people. Or maybe they're just really, really bad at explaining themselves. Who knows. We will have to wait and see what sort of contracts they actually strike in the manufacturing sector.

Monday, May 18, 2015

21

21 has announced their strategy: they've built an embeddable mining ASIC that can fit inside of any power envelope, such as a mobile phone or home router. Or even a toaster, I guess. Their revenue model is to sell the chips to manufacturers and to also collect a portion of the mining revenue the chips generate. Although 21's announcement doesn't name the revenue share number, previous rumors pegged it at 75% for 21 and 25% for the user. So in essence, you get a small discount up front in exchange for a higher electric bill, forever. This is worse than a high-APR loan from Sears for furniture. That at least ends at some point.

Of course, the announcement from 21 says that the manufacturer can also keep a share of that revenue for itself, so the true end-user could get much less than 25%. Maybe even 0%. But they will still have to pay that electric bill.

How does this pass the "good business" sniff test? Does anyone at 21 actually care about delivering value to the end users?

Essentially what users are paying for is the chip and their electric bill, and what they get is a very small stream of Satoshis (or possibly zero Satoshis). Presumably 21 is running some kind of virtual mining pool that will smooth out the mining rewards, so that everyone (or at least the manufacturer) get some small level of income. But this mining pool also presents a risk for Bitcoin. If 21 succeeds in getting its chips embedded all over the place, and they mine Bitcoins using "free" electricity from their users, then they can out-compete all other miners and possibly put them out of business. And if they approach or exceed 51% of the hashrate with this pool, Bitcoin is no longer decentralized. It would be controlled by a single US firm that could be targeted (overtly or covertly) by the US Government.

I can't say I'm excited about the ethics of the business model either. To the end user who's spending the Satoshis, they're paying a huge mark-up for the Bitcoins compared to buying their own mining rig in exchange for the convenience of having a few Satoshis on hand at all times. Between losing 75% or more of the bitcoins they mine to 21 and the company they bought the hardware from, and the fact that most end-users have more expensive electricity than the industrial miners located in Oregon or Iceland, they're essentially paying a 400% tax on the mining work they do. Is that worth it? Is that a good deal for end users? I guess it depends on how much they value convenience, and how their mining costs relate to the open market cost of BTC. But it's not obviously a deal to me.

I can see this being a good business for 21 though, at least in the short term. They sell the chips and also get the recurring revenue from the mining work for as long as the device is plugged in somewhere. But is it good for users? It feels predatory to me.

Let's look at the use-cases proposed by 21 in their blog post. Several of them are exactly the same thing, phrased different ways. I have thus grouped them categorically:

Category 1: Overpaying for Bitcoins:

Of course, the announcement from 21 says that the manufacturer can also keep a share of that revenue for itself, so the true end-user could get much less than 25%. Maybe even 0%. But they will still have to pay that electric bill.

How does this pass the "good business" sniff test? Does anyone at 21 actually care about delivering value to the end users?

Essentially what users are paying for is the chip and their electric bill, and what they get is a very small stream of Satoshis (or possibly zero Satoshis). Presumably 21 is running some kind of virtual mining pool that will smooth out the mining rewards, so that everyone (or at least the manufacturer) get some small level of income. But this mining pool also presents a risk for Bitcoin. If 21 succeeds in getting its chips embedded all over the place, and they mine Bitcoins using "free" electricity from their users, then they can out-compete all other miners and possibly put them out of business. And if they approach or exceed 51% of the hashrate with this pool, Bitcoin is no longer decentralized. It would be controlled by a single US firm that could be targeted (overtly or covertly) by the US Government.

I can't say I'm excited about the ethics of the business model either. To the end user who's spending the Satoshis, they're paying a huge mark-up for the Bitcoins compared to buying their own mining rig in exchange for the convenience of having a few Satoshis on hand at all times. Between losing 75% or more of the bitcoins they mine to 21 and the company they bought the hardware from, and the fact that most end-users have more expensive electricity than the industrial miners located in Oregon or Iceland, they're essentially paying a 400% tax on the mining work they do. Is that worth it? Is that a good deal for end users? I guess it depends on how much they value convenience, and how their mining costs relate to the open market cost of BTC. But it's not obviously a deal to me.

I can see this being a good business for 21 though, at least in the short term. They sell the chips and also get the recurring revenue from the mining work for as long as the device is plugged in somewhere. But is it good for users? It feels predatory to me.

Let's look at the use-cases proposed by 21 in their blog post. Several of them are exactly the same thing, phrased different ways. I have thus grouped them categorically:

Category 1: Overpaying for Bitcoins:

- Micropayments. You can conveniently spend Satoshis on stuff that you overpaid for in the first place. Convenience is nice, but isn't there a way to solve convenience without overcharging people for the medium of exchange? Also, the amount of money you spend is inherently constrained by the revenue generated by the 21 chip. How many articles per month or downloaded songs is that? Can't be many.

- Devices pay for services. Same as above, convenience for being badly over-charged, but instead of content your buying some service. A mesh network perhaps. Mesh networks are great. Isn't there a way to pay for them without paying the 21 tax?

Category 2: Actually not even a working feature

- Machine Twitter. Only works if they ever get Sidechains to work. I'm ignoring this for now.

Category 3: Extracting revenue from users

- Devices can pay channel partners. This is a way for manufacturers, retailers, and mobile carriers to continue to extract mining revenue from users long after the device has been sold, or is even under warranty. Yay! I'm excited about this possibility, aren't you?

- Silicon-as-a-service. This seems ridiculous. There's no way home router's single-core miner produces enough BTC revenue to pay for the miner. Maybe it's a little cheaper, like Amazon's Kindles with Ads, but not free. And the user pays for the additional electricity used, so it's more like a high-APR "payment plan" that never has they hope of getting paid off. 21 just keeps taking your bitcoins, forever.

- Bitcoin subsidized devices. This is the exact same point as previous. Why is it even a separate item on their list?

- Decentralized Device Authentication. This is possibly useful. In fact, it's the only part of the business model that seems useful to the end user. Unfortunately it's also the least fleshed out, and depends on developers of future services using the feature.

Category 4 is the only category of "features" which I consider to really be a good deal for the user. It's only useful though with widespread adoption. And widespread adoption only happens if manufacturers build the chip in. And their incentive for including the chip is only as strong as the revenue they can extract from the Category 3 features, which steals electricity from end-users. And if the channel participants keep too much of the Satoshi stream, the end user has nothing to spend, making the whole point of 21's existence worthless. I hope 21 has the sense to cap how much revenue the channels can take, otherwise the end-user ends up with nothing except a couple bucks knocked off the sticker price and a higher electric bill.

Also, let's think about the long term implications. If 21 succeeds, they will attract competitors. Mining ASICs are dirt simple to engineer. There will be a Chinese competitor to 21 within a year or two at most, and they'll compete for manufacturer share by offering a larger revenue share from the mining work. Eventually the manufacturers will have most of the bargaining power here, as they control the relationship with the end-users buying the devices. Meanwhile end users will get the mining chip that's best for the manufacturing company, not the end-user, since it's a an add-on feature most people won't care about. I don't see the situation improving for end-users over time, but it may get worse for 21.

If there's a best possible future though, it's this: 21 succeeds, Category 2 gets people using Bitcoin, and thus Category 4 gets a lot of support, and the convenience of adding Bitcoins to your wallet purchased off the open market improves, which means a real micro-payments market appears, and informed users start demanding "fair" division of bitcoins from their mining work - and some manufacturers actually deliver on that. In that future, we pay up front a fair price for our ASIC, and in return get lots of cool services and also get to keep and spend most of the Satoshis our mining work actually generates (minus only the pool operator's fee, which would be subject to market competition).

A lot of things have to go right for that to happen though, and I can just as easily see a situation where the channels take 100% of the profit from these chips and users get nothing but electric bills.

Friday, May 15, 2015

SpaceChain: A decentralized, private space program, powered by Bitcoin

In what seems to be a perfect convergence of my interests, SpaceChain (which is headed by Iman Mirboki of Sweden) is building a decentralized space program using open-source software and hardware designs, bitcoin, and crowd-sourcing. Their goals are ambitious, including putting a satellite into permanent orbit using a rocket they have built themselves. They are also integrating Bitcoin as a means for space assets (satellites, rockets, etc.) to exchange payments for services. Their proof of this concept is to launch both a satellite cargo and a fuel cargo in separate modules and then have the satellite cargo pay for a fuel transfer.

I can't tell you how exciting this is. Many folks in the Bitcoin and cryptocurrency space have talking about machine-to-machine payments as a use case for Bitcoin, and many in the space access community know that on-orbit refueling is a critical step into expanding human activity beyond low-Earth orbit in an economical way. Combining these two trends is beyond cutting edge.

In the near term I have realistic expectations of SpaceChain, which is that they won't accomplish much too quickly. Such poorly funded efforts rarely do. But still, the existence of the program at all is a testament to how the Internet + Bitcoin is changing (and will continue to change) our world, along with advances we are seeing in electronics, sensors, and robotics.

For nearly 25 years now the Internet has allowed people to organize thoughts and software code around the world, and it gave us things that couldn't have existed prior to it, like Linux and Wikipedia. Now with Bitcoin it's finally as easy to coordinate and aggregate economic value and interest on a global scale, and this will mean that decentralized teams (or even just aggregations of fans) will be able to do things requiring money that it used to require corporations or governments to organize. Kickstarter is only a first taste of decentralized economic activity, built as it is on top of the old credit card networks.

Decentralized manufacturing (3D-printing and home CNC-mills) plus advances in commodity miniature electronics thrown off by the smartphone supply chain will be the other half of this story. With the democratization of the tools of manufacturing, the hardest part of manufacturing that remains is figuring out how to build something. When that knowledge can be aggregated and shared for free across the globe, the barriers to entry and experimentation fall rapidly.

I can't tell you how exciting this is. Many folks in the Bitcoin and cryptocurrency space have talking about machine-to-machine payments as a use case for Bitcoin, and many in the space access community know that on-orbit refueling is a critical step into expanding human activity beyond low-Earth orbit in an economical way. Combining these two trends is beyond cutting edge.

In the near term I have realistic expectations of SpaceChain, which is that they won't accomplish much too quickly. Such poorly funded efforts rarely do. But still, the existence of the program at all is a testament to how the Internet + Bitcoin is changing (and will continue to change) our world, along with advances we are seeing in electronics, sensors, and robotics.

For nearly 25 years now the Internet has allowed people to organize thoughts and software code around the world, and it gave us things that couldn't have existed prior to it, like Linux and Wikipedia. Now with Bitcoin it's finally as easy to coordinate and aggregate economic value and interest on a global scale, and this will mean that decentralized teams (or even just aggregations of fans) will be able to do things requiring money that it used to require corporations or governments to organize. Kickstarter is only a first taste of decentralized economic activity, built as it is on top of the old credit card networks.

Decentralized manufacturing (3D-printing and home CNC-mills) plus advances in commodity miniature electronics thrown off by the smartphone supply chain will be the other half of this story. With the democratization of the tools of manufacturing, the hardest part of manufacturing that remains is figuring out how to build something. When that knowledge can be aggregated and shared for free across the globe, the barriers to entry and experimentation fall rapidly.

Wednesday, May 6, 2015

FinCEN fines Ripple $700k, requires remedial actions

Post updated to reflect comments from Ripple; see bottom of post.

The U.S. Financial Crimes Enforcement Network (FinCEN) has announced an enforcement action against Ripple Labs, Inc. (Ripple) and its subsidiary XRP II, LLC (XRP). This is the first enforcement action against a virtual currency company. Their findings of facts and violations include that Ripple acted as a money service business (MSB) without registering with FinCEN, and that both Ripple and XRP acted improperly. The fine is $700,000.

The rules that FinCEN found Ripple and XRP to be in willful violation of are primarily ones of anti-money laundering (AML) compliance. They did not implement their AML program quickly enough, when it was implemented it was not good enough, and a number of transactions which FinCEN deemed to warrant the filing of suspicious activity reports (SARs) did not get filed. These are the sort of violations that any exchange (whether dealing in virtual currencies or strictly fiat ones) might commit.

The remedial actions required by FinCEN are what seem to be causing the most conversation on Twitter and similar online discussion forums.

A lot of it is exactly what you'd expect. There's the $700,000 fine, a requirement that Ripple and XRP implement better AML practices, and the requirement of a third-party auditor for the next six years to verify that the AML program is in place and being followed appropriately. There's also a requirement to look back at the last three years of data available to Ripple and file any SARs that such information may warrant.

Further however the remedial actions may require (but it's not entirely clear) updates to various parts of the virtual currency software developed by Ripple. This is not the software and business logic used internally at Ripple or XRP to run their businesses, but the software that runs the Ripple protocol and network.

Let's take a look at some of the requirements specifically.

An important thing to note is that both Section 8 and Section 10 are only possible because Ripple runs on a shared, transparent ledger (like Bitcoin). There is no equivalent to "monitor across the entire protocol" in regular banking, because there is no shared ledger. Everything has to happen at the individual bank level. FinCEN is leveraging the existence of the shared ledger to get better information than they normally could get from any single firm, and they're having Ripple do the development work form them. This certainly shows they understand how the new technology is different from the old technology, and how it creates opportunities for FinCEN as a regulator.

Okay, last section:

The requirement that all "transactions" be compliant with the travel rule implies to me that Ripple Trade will have to be updated to to disallow transactions where the requirements are not net. This further implies that assets can only be transferred out of Ripple Trade or Ripple Wallet if they are being sent to another compliant wallet.

A question of what a "compliant wallet" is remains open. Is it sufficient that a wallet promise to provide and receive the necessary information? What if it becomes common knowledge that one particular wallet host is lousy about keeping records? I doubt FinCEN would be happy with that, which further implies some sort of whitelist for wallets.

[SEE UPDATE BELOW] The last point to raise is this speech by FinCEN Director Calvery, given today. In it she says:

UPDATE: The BitBeat blog reports that the protocol will not be updated after all. The following statements come from Ripple:

The other interesting point is this:

The U.S. Financial Crimes Enforcement Network (FinCEN) has announced an enforcement action against Ripple Labs, Inc. (Ripple) and its subsidiary XRP II, LLC (XRP). This is the first enforcement action against a virtual currency company. Their findings of facts and violations include that Ripple acted as a money service business (MSB) without registering with FinCEN, and that both Ripple and XRP acted improperly. The fine is $700,000.

The rules that FinCEN found Ripple and XRP to be in willful violation of are primarily ones of anti-money laundering (AML) compliance. They did not implement their AML program quickly enough, when it was implemented it was not good enough, and a number of transactions which FinCEN deemed to warrant the filing of suspicious activity reports (SARs) did not get filed. These are the sort of violations that any exchange (whether dealing in virtual currencies or strictly fiat ones) might commit.

The remedial actions required by FinCEN are what seem to be causing the most conversation on Twitter and similar online discussion forums.

A lot of it is exactly what you'd expect. There's the $700,000 fine, a requirement that Ripple and XRP implement better AML practices, and the requirement of a third-party auditor for the next six years to verify that the AML program is in place and being followed appropriately. There's also a requirement to look back at the last three years of data available to Ripple and file any SARs that such information may warrant.

Further however the remedial actions may require (but it's not entirely clear) updates to various parts of the virtual currency software developed by Ripple. This is not the software and business logic used internally at Ripple or XRP to run their businesses, but the software that runs the Ripple protocol and network.

Let's take a look at some of the requirements specifically.

Within 30 days of the date of this agreement, Ripple Labs and XRP II will move its service known as Ripple Trade (formerly known as Ripple Wallet, which allows end users to interact with the Ripple protocol to view and manage their XRP and fiat currency balances), and any such functional equivalent, to a money services business that is registered with FinCEN (the “Ripple Trade MSB”).So the wallet needs to be run out of the FinCEN registered MSB. I'm surprised this isn't already the case, but maybe it's a question of formally moving ownership of Ripple Trade from Ripple to XRP (the latter is registered currently).

Users of Ripple Trade (which will include all users registering after the date of this agreement and any existing users who register at the request of Ripple Labs) will be required to submit customer identification information, as required under the rules governing money services businesses, to the Ripple Trade MSB;This seems a lot like what Coinbase and Circle already require today in the Bitcoin world. One thing that's different however is that, per the Ripple Terms of Use (see Item 3), Ripple Trade does not have access to user keys. They're a web-based wallet like Blockchain.info. This indicates that while wallets that lack keys to your accounts may not have the same level of fiduciary obligations as a hosted wallet like Coinbase, they still have AML obligations under FinCEN rules.

After 180 days of the date of this agreement, Ripple Labs will (1) prevent any existing Ripple Trade user who has not transferred to a wallet or account with customer identification information from accessing the Ripple protocol through the Ripple Trade client, and (2) not otherwise provide any support of any kind to such a user in accessing the Ripple protocol.So, 180 days from now, any Ripple Trade account which is not AML-compliant will be frozen. Interestingly this requirement doesn't just say that they cannot trade with Ripple Trade. It says the account cannot be allowed access to the Ripple protocol. If they cannot access the protocol then they cannot move the money to another wallet or a personal wallet. The money is just stuck there until they meet the reporting requirements.

8. Enhancements to Ripple Protocol: Within 60 days, Ripple Labs, XRP II, and the Ripple Trade MSB will improve, and upon request provide any information requested by FinCEN or the U.S. Attorney’s Office as to the use and improvement of, existing analytical tools applicable to the Ripple protocol, including: (1) reporting regarding any counterparty using the Ripple protocol; (2) reporting as to the flow of funds within the Ripple protocol; and (3) reporting regarding the degree of separation.I am admittedly not as familiar with the Ripple network as I am with Bitcoin. I'm not sure what sort of blockchain analysis (if that's even the right word) is possible on Ripple. But this requirement seems to be saying that Ripple will build the tools necessary to do blockchain analysis that can positively identify any counterparty and follow the flow of funds between parties. No doubt there will be some connection between these tools and the AML-required customer information collected.

10. Transaction Monitoring: Ripple Labs will institute AML programmatic transaction monitoring across the entire Ripple protocol, and will report the results of such monitoring to the U.S. Attorney’s Office, FinCEN, and any other law enforcement or regulatory agency upon request. The monitoring and reporting must include, at a minimum: (a) risk rating of accounts based on the particular gateway used; (b) dynamic risk tools to facilitate investigation of suspicious activity, including counterparty reporting, flow of funds reporting, account flagging of suspicious accounts, and degrees of separation reporting; and (c) other reports of protocol-wide activity regarding any unlawful activity.More monitoring and blockchain analysis, this time (I think) for "programmaticaly" identifying accounts and activity which warrant a SAR being filed.

An important thing to note is that both Section 8 and Section 10 are only possible because Ripple runs on a shared, transparent ledger (like Bitcoin). There is no equivalent to "monitor across the entire protocol" in regular banking, because there is no shared ledger. Everything has to happen at the individual bank level. FinCEN is leveraging the existence of the shared ledger to get better information than they normally could get from any single firm, and they're having Ripple do the development work form them. This certainly shows they understand how the new technology is different from the old technology, and how it creates opportunities for FinCEN as a regulator.

Okay, last section:

11. Funds Travel Rule and Funds Transfer Rule: XRP II and the Ripple Trade MSB will ensure, or continue to ensure, that all transactions made using XRP II, Ripple Trade, or Ripple Wallet will be, or will continue to be, in compliance with the Funds Transfer Rule and the Funds Travel Rule.The "Funds Transfer and Travel Rules" requires that one financial institution (including, in this case, Ripple Trade and Ripple Wallet) must pass on certain information to the next institution (or wallet) for certain kinds of transactions. Essentially, Ripple can't just send your XRP to Joe Wallet Co., it also has to send them your name and address.

The requirement that all "transactions" be compliant with the travel rule implies to me that Ripple Trade will have to be updated to to disallow transactions where the requirements are not net. This further implies that assets can only be transferred out of Ripple Trade or Ripple Wallet if they are being sent to another compliant wallet.

A question of what a "compliant wallet" is remains open. Is it sufficient that a wallet promise to provide and receive the necessary information? What if it becomes common knowledge that one particular wallet host is lousy about keeping records? I doubt FinCEN would be happy with that, which further implies some sort of whitelist for wallets.

[SEE UPDATE BELOW] The last point to raise is this speech by FinCEN Director Calvery, given today. In it she says:

Ripple Labs will also undertake certain enhancements to the Ripple Protocol to appropriately monitor all future transactions.My initial (and definitely not legal advice!) reading of Ripple's remedial action requirements didn't see any requirement that the protocol be updated - despite Section 8 being called "Enhancements to Ripple Protocol". The closest change I see to a protocol-level change would be Section 11, but even the Travel rule could be enforced at the wallet level (not the protocol level). The actual text of the remedies implies enhancements to monitoring software and wallets. But Director Calvery seems to think the protocol will be changed. I could plausibly speculate a number of reasons for this being the case (loose language, last minute changes to the settlement, technical non-clarity at FinCEN, etc.), but right now it's just not clear what this means.

UPDATE: The BitBeat blog reports that the protocol will not be updated after all. The following statements come from Ripple:

All that Ripple had agreed to, [Ripple Labs’ new Bank Secrecy Act officer, Antoinette O’Gorman] said, was to build enhanced “analytical transaction monitoring tools for monitoring transactions across the protocol” and to furnish information drawn from that monitoring to U.S. authorities upon request. The changes had “nothing to do with the protocol itself,” she said.

These monitoring tools are secondary applications that anyone could have built to analyze the flow of data across the publicly transparent ledger of Ripple transactions, she said.Okay, so it's blockchain analysis tools, as I speculated above. This reinforces my point that FinCEN is taking advantage of the unique nature of transparent, decentralized ledgers to see further onto the flow of funds than a bank-by-bank approach would allow.

The other interesting point is this:

Addressing another contentious point, Ms. Gorman said her company had argued that Ripple Trade, a wallet application with which people can view and manage their balances of XRP, Ripple’s native currency, should not be registered as a money service business, or MSB, under FinCEN rules because it was merely a software tool without power to take custody of funds or directly exchange currency. However, FinCEN was insistent, demanding that Ripple Trade be migrated to a properly registered MSB, which means that its users must submit customer identification information.I would like to know more about FinCEN's basis for this demand. Is FinCEN is going down the road that software which allows financial activity must be hosted by regulated companies (where users must disclose identifying information)? Or did they just ask for what they thought they could get? With the issues around whether the protocol is being changed being resolved in the negative, this part is now the biggest open question raised by this action.

Subscribe to:

Posts (Atom)